The Micron Minute: Can DRAM Prices Really Double From Here?

A new column focusing on Micron and the ever changing memory market

New Column, Who Dis?

I decided this week to change things up a bit, and instead of my Thursday What I’m Watching column, I thought I’d start a brand new column focusing on the semiconductor Micron MU 0.00%↑.

Many of my readers, especially long-time readers, found me through my Micron writing and podcasts. I’ve been writing on Micron since September 2015, when I found it in the dumpster bin of the market. Things were looking dour for the memory producer as DRAM prices were in free fall. But something about the underdog vibes brought me to not only covering it but owning it. Ten years later, not only do I still own it, but it’s one of a few stocks I’ve covered consistently and with a depth I didn’t think was possible. I know it so intimately I can recall most of the facts off the top of my head and do a TED talk on it. It’s also grown to my top three holdings in my portfolio.

If this column resonates with my readers, I may replace my Thursday What I’m Watching article with the Micron Minute. Of course, you’ll still get Monday’s What I’m Watching, but I think this’ll break up my offerings for my free readers, and even paid readers, with more timely information.

The idea in this column isn’t to cover Micron incessantly, or even solely. Because Micron operates within the memory industry, wide-ranging questions can be answered for other companies, including Sandisk SNDK 0.00%↑, Western Digital WDC 0.00%↑, Seagate STX 0.00%↑, Samsung, SK Hynix, among others. DRAM and NAND aren’t a Micron-only application, and thus, the information I share here should allow you to bring research to your other investments. It’s also not intended to delve deep into Micron or the memory industry each week; it’s meant to be an update column with the news over the past week, or to discuss a resurgent topic from recent events.

CEOs Are Commenting On The Historic Nature Of This Memory Cycle

For today’s installment, I want to cover recent comments about the DRAM environment coming from a few CEOs in the industry.

One that caught my attention is from the ADATA Chairman, Simon Chen. He stated the “grain bins” of the three DRAM memory producers are “nearly empty.” He went on to say, “Our competitors in securing supply are no longer our peers in the industry - they are now the cloud service provider (CSP) giants.”

In order to understand his last statement, you have to understand where ADATA is in the supply chain.

ADATA is a memory module maker, producing DRAM modules, flash drives, HDDs, and SSDs. This means ADATA relies on the likes of Micron, SK Hynix, and Samsung to provide it with the DRAM and NAND chips it needs to package them into the component destined for the end product. For DRAM, this is a module that then goes into the device further down the supply chain. One such form factor looks like this:

Those chips on the module are sourced from one of the three major DRAM producers. So in order for ADATA to sell its products, it needs supply from one, if not all, of the three producers.

With that in mind, what does Chen mean about competing to secure supply outside of peers? What shifted to make them go from non-competitors to competitors?

Chen is referring to the large cloud providers like Google GOOGL 0.00%↑ GOOG 0.00%↑, Amazon AMZN 0.00%↑, Microsoft MSFT 0.00%↑, and Meta Platforms META 0.00%↑, to name a few, not to mention the direct data center builders now, such as OpenAI, CoreWeave CRWV 0.00%↑, and others.

Previously, these large cloud providers bought servers from OEMs that built these systems. But because the CSPs require so much capacity, they are ordering components themselves, right down to the DRAM chips. Though I assume that’s not their main product purchase, but instead assembled modules directly from Micron, SK Hynix, and Samsung. Either way, that’s inventory the three producers don’t have to supply ADATA.

Now, one might think it’s difficult to assume this is for DDR5 and the latest technology, as DDR4 is at end of life (EOL). DDR4 would absolutely have very little supply, as the big three producers said they were winding down DDR4 operations. However, CSPs aren’t buying DDR4; they’re buying DDR5 to power their data centers, which run on DDR5 and (now) high-bandwidth memory (HBM).

Speaking of HBM, why is HBM relevant?

Supply to traditional DDR5 components is also in short supply, as the three memory producers push their efforts toward the higher-margin HBM market. Thus, not only is DDR4 scarce and close to non-existent, but DDR5 is getting squeezed out by the high-performing AI memory. HBM and DRAM for DDR5 use the same basic technology. The difference comes from form factors, packaging, and throughput, but the same 1-beta transistor technology node producing wafers for DDR5 is the same technology used for HBM. This means bits are being pulled into a non-DDR5 direction, lessening the supply there. Not to mention it takes three times as many bits to produce HBM as it does DDR5.

And since the memory market is in an upcycle, supply expansion to this point has been restrained, leading to demand exceeding supply at a foundational level, let alone the inter-industry dynamic I just described.

ADATA has allegedly told its sales team to “sell sparingly and prioritize key customers.” A sales team that can’t sell, now there’s proof of a shortage.

That’s a problem for anyone looking to procure memory components.

Before I go into what this means practically for DRAM pricing, let’s read what the big three DRAM producers have to say on the topic, too.

Micron just had its earnings call a few weeks ago, where it stated demand in the data center, across traditional and AI, has been exceptionally strong:

Robust data center demand, including the uptick in server unit growth has contributed to a tight industry DRAM environment and strengthened NAND market conditions. Additionally, broadening of demand across end markets has also constrained DRAM supply.

…

In calendar 2026, we anticipate further DRAM supply tightness in the industry and continued strengthening in NAND market conditions.

Sanjay Mehrotra, CEO, Micron’s FQ4 ‘25 Earnings Call

The result is DRAM is tight right now and is only going to get tighter in 2026.

SK Hynix and Samsung mirror this sentiment, saying the DRAM market has gotten tighter as AI demand accelerates, and traditional server and consumer end markets increase their demand.

What This Means Practically For Supply

So, is this enough to continue the significant increase in DRAM pricing we’ve seen over the last year?

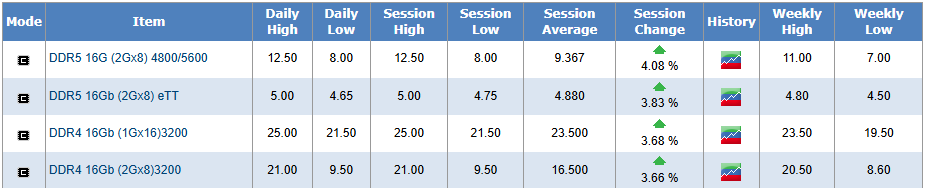

Well, we continue to see spot prices up daily with more than trivial moves.

But DRAMeXchange has become irrelevant in the data center-driven days we’re seeing now in 2025. Moreover, spot prices are irrelevant to much of the industry as the industry moves on contract prices. Some will say spot influences contract, but in the more specialized era of DRAM products, the producers are dictating pricing more than they ever have with direct contracts and customization, especially with HBM.

Thus, following spot prices is a worthless endeavor.

Following contract prices is the better option, but DRAMeXchange posts PC and consumer contract prices. For Micron, consumer DRAM has shrunk in terms of overall makeup of revenue as data center revenue made up 56% of total revenue in FY25. Thus, tracking DRAM pricing week-to-week or month-to-month has become increasingly more opaque. I wind up relying on my own calculations based on company insight with percentage changes quarter-to-quarter. My charts with this data are reserved for paid subscribers.

But let’s answer the question: can DRAM pricing double in the year ahead beyond what it has already grown?

Considering the industry is just now entering the higher demand part of the cycle and inventories are already falling (see below chart), the position of seeing prices increase significantly, up to 100% or more in the next year, is becoming more and more sane. Producers have allegedly suspended DRAM price quotes for DDR3 and DDR4, but it’s for reasons different than DDR5, since the older two generations are coming up on EOL.

But it doesn’t mean the DDR5 side of the industry isn’t also seeing shrinking supply amid growing demand. Producers like Micron have been upfront its bit supply growth will come mainly from node transitions, as it now sets its sights on its 1-gamma node for all things DRAM except for HBM. HBM will remain on 1-beta, helping push its non-EUV node toward HBM more fully.

Therefore, wafer starts will be reduced, all else being equal, as 1-gamma will gain bits only through die size reduction on the wafer. Because of the additional footprints for each node, wafer lines have machines added, which reduces the lines available to start wafers. However, the die size reduction is meaningful, with a 30% increase in bit density per wafer.

Micron 1γ 16Gb DDR5 product shows a better than 30% increase in bits per wafer over our 1β (1-beta) 16Gb DDR5 product.

But this is a decrease over the last node transition - going from 1 alpha to 1-beta yielded “over 35% bit density improvements.”

This isn’t unexpected. As nodes progress, the ability to fit more bits on a die decreases.

And with the idea to put as much supply behind HBM as possible (higher margins), the bits going to DDR5 components are slowing in their ability to expand supply.

What This Means For Pricing

All of these factors I’ve talked about in this article combine to prove supply isn’t coming to save the memory market anytime soon. And because there will continue to be supply and demand imbalances, prices will continue to move up. The only way the memory market comes back into balance over the next year is if demand slows.

With the intent of the world moving further toward AI to produce more efficient products and reduce labor costs, there’s no reason to slow spending and reduce demand for memory components.

We’re just now seeing the curve of DRAM pricing inflect, and I expect there to be a long tail to the pricing momentum. So, even if nothing else changes, the effects from 2025 will be felt in 2026. If demand ticks up further, expect 20% increases quarterly to be the norm.

Micron’s FQ4 ‘25 exceeded that mark already. And with blowout guidance for FQ1 ‘26, you can bet pricing will increase as much or more for DRAM in the current quarter. Just two 25% price increase quarters back-to-back is a 56% price increase from the baseline. And that’s only six months.

Overall, Micron’s leverage has never been better as it has a kingpin in HBM with sold-out supply, while it and the industry have caused its own DDR5 shortage due to it. The producers have never been in a better environment. And thus, pricing may make its way back to 2018 levels.